How to Calculate Cost of Goods Sold

Article last updated:

Article first published:

Learn all you need to know about Cost of Goods Sold, one of the most important metric businesses have to report in the Profit and Loss statement.

- What is the Cost of Goods…

- How to Calculate Cost of…

- Like what you're reading?

- What are Cost of Goods So…

- Extended COGS Formula

- Smart Tips for Calculatin…

- Changes in COGS/ How to V…

- Interpreting Your Busines…

- COGS Metrics and Ratios

- Cost of goods sold versus…

- Why Is It Important to Kn…

- What are the Limitations…

- Frequently asked question…

Cost of Goods Sold represents the direct costs linked to producing or purchasing the items a business sells. The calculation includes expenses (raw materials, direct labor costs). The process excludes indirect expenses (rent, marketing, and administrative salaries). Accurate measurement remains critical to determining gross profit and taxable income. Managers track the figure to evaluate production efficiency. The mathematical process involves combining the beginning inventory with purchases and subtracting the ending inventory. Many accounting systems automate the calculation to maintain financial records. Business owners rely on the metric to set prices effectively. A high value relative to revenue indicates potential issues in the supply chain. Understanding the data helps in improving profit margins. Consistent monitoring leads to better inventory management. The figure appears on the income statement to reduce total revenue. Precise records ensure compliance with tax regulations. Companies use different methods (FIFO, LIFO, average cost) to value inventory. Fluctuations in the amount reflect changes in material prices or labor rates. Financial health depends on maintaining a sustainable balance between production costs and sales price. Calculating the metric reveals the true cost of doing business. The process demonstrates the relationship between inventory and revenue. Analyzing the data improves the cogs calculation. Mastering the steps clarifies the cogs formula.

What is the Cost of Goods Sold (COGS)?

Cost of Goods Sold (COGS) represents all costs involved in producing goods that a company sells over a certain period of time. The cost of goods sold, known as the cost of services or the cost of sales, includes the cost of materials used to create the goods and the cost of direct labor (employees’ salaries).

COGS are used by businesses that create products, including digital goods sold online. Besides that, companies in the service industry also use COGS in the form of cost of revenue.

How to Find Cost of Goods Sold?

Cost of Goods Sold is found by collecting data from the balance sheet and income statement. Finding the figure requires gathering specific data points during the period (beginning inventory value, total purchases, ending inventory value). The process starts by identifying the beginning inventory at the start of the fiscal year. Businesses add the value of additional goods purchased or manufactured during the specified timeframe. Subtracting the ending inventory value at the conclusion of the period yields the final amount. Freight costs and direct manufacturing labor belong in the total. Accounting departments retrieve the numbers from the ledger and inventory management systems. Periodic inventory systems require physical counts to verify the ending balance. Perpetual systems update the values automatically after every transaction. Managers use the data to calculate gross profit margins and assess operational efficiency. Consistent tracking prevents discrepancies in financial reporting. High-volume businesses (supermarkets, apparel retailers) monitor the figure daily to adjust procurement strategies. Small enterprises (boutiques, local bakeries) evaluate the metric monthly to maintain profitability. Precise documentation ensures tax deductions remain accurate. Analysts compare the results across different fiscal quarters to detect trends. Effective management of the figures enhances the overall cogs formula with sales. Improving the speed of product movement depends on maintaining a high Inventory Velocity.

How to Calculate Cost of Goods Sold?

Apply the following formula to calculate the cost of goods sold.

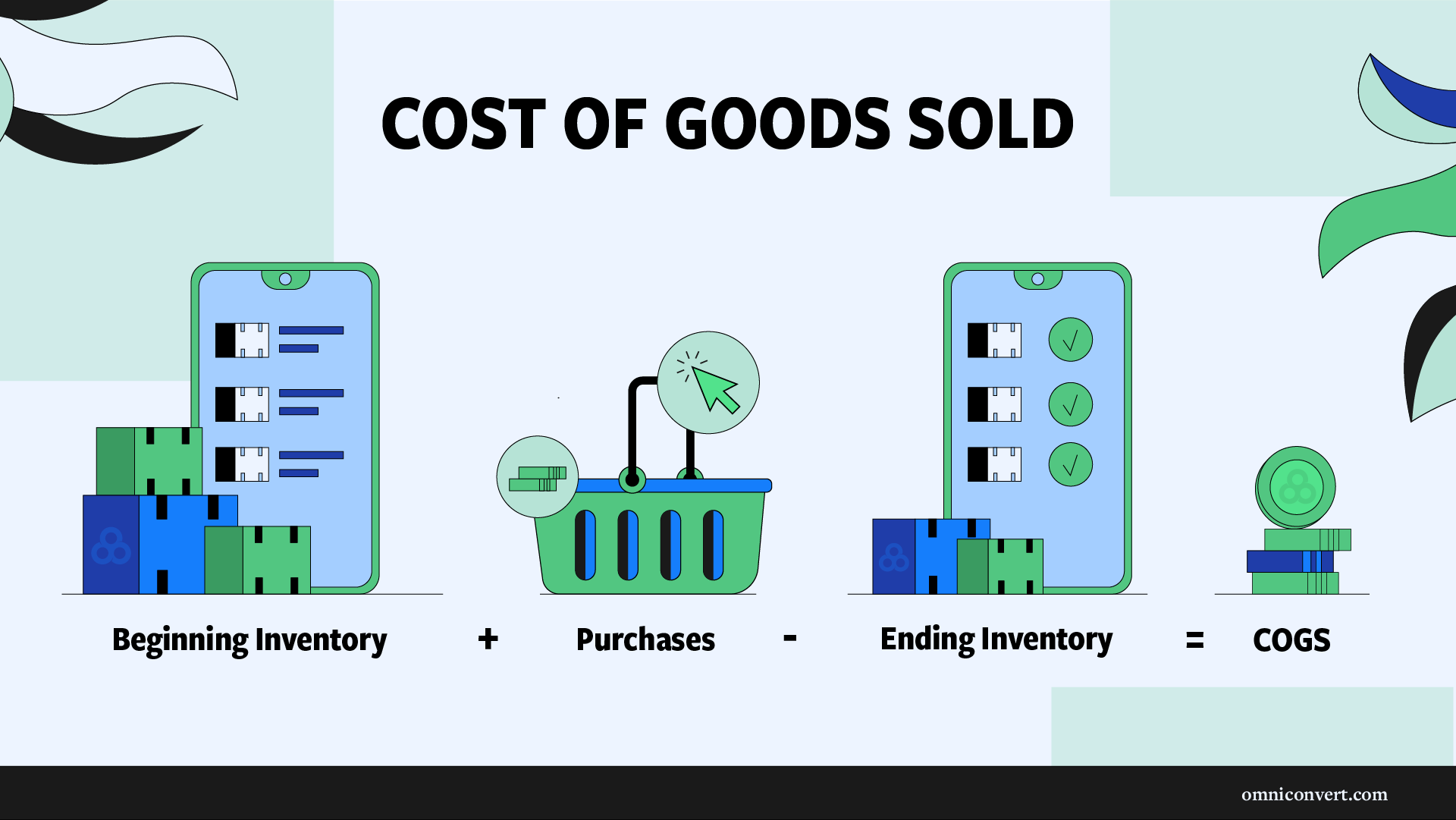

COGS = beginning inventory + purchases - ending inventory

Let’s take a quick look at the components of COGS:

- Beginning inventory: Beginning inventory is the company's inventory from the previous period. It could be the previous quarter, month, year, etc.

- Purchases: Purchases are the total costs of what the company purchased during the specified accounting period.

- Ending inventory: The inventory that remained during that period.

COGS includes direct costs like materials and labor but leaves out indirect expenses such as marketing and sales costs.

What is Cost of Goods Sold Equal To?

Cost of Goods Sold is equal to the beginning inventory plus net purchases minus the ending inventory. The equation accounts for direct materials and labor consumed during the production process. Beginning inventory represents the value of unsold goods carried over from the previous accounting period. Net purchases include the cost of raw materials and finished items bought for resale. Ending inventory consists of the products remaining in stock at the end of the current period. The components connect directly to the balance sheet and the income statement. Direct labor costs (factory worker wages) increase the total value. Manufacturing overhead (utilities for the production facility) contributes to the direct cost of items. Indirect expenses (sales team commissions, office rent) stay separate from the calculation. Businesses use the formula to determine the gross profit during a specific duration. Consistent application of the method ensures financial transparency. Different inventory valuation methods influence the final number. A rising total suggests increased production volume or higher material prices. Maintaining accurate counts remains necessary for reliable results. The equation provides the foundation for determining the taxable income of a corporation. Clear definitions of each variable prevent accounting errors. Mathematical accuracy supports sound financial planning.

Like what you're reading?

Join the informed eCommerce crowd!

Stay connected to what’s hot in eCommerce. We will never bug you with irrelevant info.

What are Cost of Goods Sold Examples?

Cost of Goods Sold examples exist in retail, manufacturing, and the service sector. A local bookstore starts the month possessing $5,000 in inventory. The owner purchases an additional $2,000 worth of books. Ending inventory at the month's end totals $3,000. The calculation (3,000. The calculation( 5,000 + $2,000 - $3,000) results in 4,000. A furniture manufacturer itemizes raw wood ($4,000). A furniture manufacturer itemizes raw wood (500), screws (20), and direct labor (20), and direct labor(300) per table. Selling 15 tables results in a total of $12,300. Service companies selling physical products (hair salons selling shampoo) track the purchase price of the bottled goods. A salon buys 50 bottles at ten $ each and sells 40 bottles. The amount totals $400 during the period. The scenarios illustrate the direct relationship between stock levels and sales volume. Accurate records help businesses understand the profit per unit. Comparing the numbers helps in identifying waste or theft in the warehouse. Modern software simplifies the tracking of every item sold. Retailers use the insights to negotiate better prices with suppliers. Small changes in material costs impact the final profit meaningfully. Understanding the direct expenses clarifies every cost of goods sold example. Adapting to modern consumer habits reflects the ongoing Evolution of Retail.

Example 1

Let's say wanted to calculate the cost of goods sold in the first quarter of 2025. The inventory record's beginning inventory will be on 1st January and ends on March 31. If the business had a beginning inventory of $20,000 and the purchases totaled to $9,000 for that quarter, and had an ending inventory of $5,000, then the total COGS for that quarter will be:

COG= Beginning Inventory + Total Purchases on the Specified Period - the Ending Inventory

COG= $20,000+ $9,000 -$5,000 = $24,000

Therefore, the total costs of goods (COG) sold in that quarter are $24,000.

Example 2

The beginning inventory recorded for the fiscal year ended in 2020 is $3,000. There is an additional inventory purchased during the 2023-2025 fiscal year, amounting to $2,000, and $1500 ending inventory recorded at the fiscal year ended 2025. Based on the COG formula, the cost of goods sold will be:

COG=$3,000 + $2,000 - $1,500 = $3,500.

Example of a Cost of goods sold worksheet (COGS Worksheet)

Example 3

Suppose running a clothing store. The inventory of clothing is valued at $30,000 at the start of the year. The purchase an additional $50,000 worth of new stock during the year. Having $20,000 worth of clothing left unsold by the end of the year. Here’s how to calculate the COGS:

COGS=$30,000+$50,000−$20,000=$60,000

The cost of goods sold for the year would be $60,000. It includes all the inventory purchased minus what is left at the end of the year, indicating how much was sold during the year.

Example 4

A software company might seem less intuitive because it deals with digital goods, which do not have physical inventory. The costs are considered part of COGS if the company licenses third-party technologies or incorporates purchased codebases. The beginning inventory of licenses was $5,000, additional licenses bought were $25,000, and the ending value of licenses was $10,000, the COGS would be:

COGS=$5,000+$25,000−$10,000=$20,000

It reflects the cost of the licenses used to deliver sold products over the year.

Example 5

The COGS includes the cost of ingredients and food items that are used to make meals for customers in a restaurant. Let's say the beginning inventory of food supplies is $8,000, the restaurant buys $70,000 worth of ingredients during the year, and the ending inventory is $7,000. The COGS would be:

COGS=$8,000+$70,000−$7,000=$71,000

The calculation shows the cost of the food ingredients used in meal preparation throughout the year.

Extended COGS Formula

To capture a more complete picture of the production costs, it is crucial to consider additional variables that affect the bottom line. The extended COGS formula incorporates key elements such as returns, freight charges, discounts, and allowances, providing a detailed calculation that reflects the true cost of goods sold more accurately. Businesses ensure a more precise financial analysis and make informed decisions to enhance profitability by including the factors. Here's how each component plays a crucial role in the formula:

COGS = Beginning inventory + purchases + Freight In - Ending inventory - Purchase Discounts - Purchase Returns and Allowances

- Beginning inventory: Beginning inventory is the inventory amount at the opening of the stock period.

- Purchases: Any costs incurred for purchasing manufactured products or setting up a product, for instance, raw materials.

- Freight In: The transport costs incurred for the raw materials being brought to the setup location or factory.

- Ending inventory: The amount of closing stock for the specified period.

- Purchase discounts: Purchases are discounts that are received in the product supply chain.

- Purchase returns and allowance: Purchase returns are costs incurred when items are returned to suppliers. Allowances are any additional benefits that are received in the product's purchase chain.

Here’s an example that demonstrates how to apply the Extended COGS Formula in a practical scenario.

Consider a company XYZ manufacturing packet of pens. Note that the direct cost of manufacturing one packet is $2.00, and below are the other statistics.

- Opening inventory: 3000 packets

- Closing inventory: 1,000 packets

- Freight in $20,000

- Discounts received: $4,500

- Purchase costs: $50,000

Solution The cost of opening inventory: 3000 x 2 = $6,000 The cost of closing inventory: 1000 x 2 = $2,000 COG= $6,000 + $50,000+ $20,000-$4,5000 - $2000 = $69,500.

The solution calculates the total COGS for a company manufacturing packets of pens by utilizing specific data such as opening and closing inventory, freight costs, discounts, and purchase expenses. The illustration aims to offer readers a clear understanding of how the formula works in real-world contexts, aiding them in their financial analysis and decision-making processes.

> Discover the top 10 KPIs that have a major impact on your Customer Lifetime Value.

Smart Tips for Calculating COGS Accurately

Smart tips for calculating COGS accurately are listed below.

- It's crucial to understand the difference between direct and indirect costs when calculating the COGS. Direct costs are directly tied to production, like raw materials and labor used on the product line. Indirect costs, which shouldn’t factor into your COGS, include things like salaries for staff who don't work on the production line, rent for your office spaces, and depreciation of non-production assets.

- Keep tabs on your beginning inventory. The starting inventory at the beginning of the year must match the ending inventory from the previous year. The consistency ensures accuracy in your year-over-year cost tracking.

- Returned goods directly affect your COGS calculation. Ensure proper accounting for all returns and allowances. Deduct from the total sales to prevent overstating the revenue, which, in turn, adjusts your COGS for goods that were not actually sold.

- The method used for inventory valuation (e.g., FIFO, LIFO, Average Cost) affects the COGS calculation. Consistently applying the same accounting method is crucial for accurate financial reporting and comparison across periods. Switching methods can lead to significant variations in COGS, affecting financial analysis and forecasting.

- Changes in supplier pricing affect the COGS. Regular monitoring of the changes helps anticipate impacts on the cost structure. Monitoring is particularly important for businesses where raw materials constitute a large portion of COGS. Timely adjustments in pricing strategy or sourcing decisions be necessary to maintain profitability.

Changes in COGS/ How to Value Your Inventory

There are three types of inventory costing techniques that you can use to value your inventory:

First In, First Out (FIFO)

Goods that were manufactured or purchased first are the first ones to be sold. It means that the business will have to sell first the least-expensive products with FIFO inventory. That's why this method usually results in lower COGS.

Last In, First Out (LIFO)

Opposite of FIFO, it assumes the last items purchased are the first sold. Useful in reducing income tax during inflation, but leads to higher COGS.

Average Cost

The method smooths out price fluctuations by averaging the cost of goods available for sale during the period.

Note: Regardless of the inventory method chosen, it is important to find a technique that works for the business and stick to it. It will help to ensure calculation consistency. It will bring in familiarity and help quickly determine possible calculation errors.

Interpreting Your Business's COGS

Now that you know the information relayed by COGs, what does this mean to your business? The first thing you need to realize is that COGS is critical in determining the operational efficiency of the business. COGS helps quickly pinpoint the parts of the production process that increase the operational costs.

It will reduce operational costs by minimizing the staff, reducing machine idle time, or implementing new business tactics. Using COGS promote operational efficiency by:

- Trying to minimize thefts and product damage in the best way possible

- Avoiding overstocking to avoid losses and increased warehousing and storage costs

- Getting enough stock to avoid last-minute orders or loss of revenue

Apart from production efficiency, the formula is ideal for comparing the costs of different products. Such information helps identify products that bring in more money and result in losses for companies dealing with multiple products.

A business appear efficient yet still report an extremely high cost of goods sold, which signals product-level inefficiencies rather than operational failure. A multi-product business benefits from reviewing item-level margins and discontinuing products that carry disproportionately high COGS.

COGS Metrics and Ratios

To effectively determine the number of goods sold for a business and its financial health, the ratios and metrics that be used with COGS are:

COGS Ratio

It is used to highlight the sales revenue percentage used by businesses to pay for the expenses that directly vary with sales.

COGS ration = (COGs/ Net Sales) x 100

For instance: if a Company Z has COGS of $50,000 and total net sales of $60,000, then its COGS ratio will be:

(50,000/60,000) x 100 = 83.3%

Inventory Turnover

It is a type of ratio used to determine how well a company can generate sales from its inventory. Inventory turnover indicates the number of times that the involved company has sold and replaced its inventory in a given period. To calculate it:

Inventory formula = COGS/ Inventory Average

The average of any inventory can be established by adding the ending and beginning of the inventory and then dividing this amount by two. High inventory turnover is proof of more sales and moderately good inventory.

Gross Profit Margin

It is the percentage of sales revenue a company retains after incurring all its COGS. It must be noted that the higher the gross margin, the more the amount a business can retain from every dollar of revenue.

Gross margin = ((Sales revenue - COGS) / Sales Revenue) x 100

> Discover how to promote your best products using the Product Assortment Optimization Framework.

Cost of goods sold versus operating expenses

To understand the difference between operating expenses and the costs of goods sold, you must take into account how you attribute said costs.

Operating expenses the expenses that aren't directly tied to creating the product. These can include rent, administrative fees, office supplies, etc. The majority of your costs will go under this category.

COGS, on the other hand, refers strictly to the costs directly involved in producing the goods: the materials you used, delivery, labour, etc.

Why Is It Important to Know COGS?

Understanding COGS is essential for small business owners for the following reasons:

Setting the right product price

Setting the right product price to know the COGS, set up the correct product cost without deterring your customers. With the right price will be able to successfully cover its operating costs while ensuring that earn a healthy profit margin. It will be in a good position to know when to reduce or increase the product prices. Use COG alongside other industry-approved techniques to ensure that it effectively compete with other businesses in the same niche.

Managing Your Taxes

Managing taxes is a direct relationship between your COGS and your taxes. Note that sold COGS for the business are tax-deductible. COGS are usually the second line item that appears in the income statements of companies. Business owners don't want to get into legal disputes for not correctly filing the taxes.

If the business has high COGS will pay less in taxes with lower net income. It will be a highlight in alerting that the business is highly likely not making enough profit, it needs to implement a system that creates a healthy balance between its business's profitability and operational costs.

Detecting Growth Opportunities

Consistently using COGS means using the historical data attained to determine seasonal trends. It identifies new opportunities that will drive the growth of your business by using historical changes. If your COGS is higher in winter, diversify of the business with products in demand in winter to minimize the risk of making losses.

Analyzing Your Business's Health

Analyzing business health uses COGS to calculate different ratios, which means that it conveniently determines the business's health. Making better decisions, especially for owners more likely to impact the business positively. The obtained information helps figure out if the business must try to reduce operational costs, if fully pay the debts, or if it must consider closing down the business.

If an eCommerce business is looking for a way to unlock significant data-driven growth, then it should consider using REVEAL. The software program organically increases the number of customers loyal to your business. It provides actionable insights on how you maximize profits and helps to improve customer lifetime value.

The high-performance software program is already being used by more than 2200 brands, including Decathlon, Heineken, Culture Kings, Your Super Foods, etc. REVEAL's main features include:

- Customer analytics and segmentation

- Product performance

- Customer experience

- Integrations

- eCommerce analytics

If ready to improve the e-commerce customer lifetime value, then get REVEAL now on Shopify or other platforms.

Are There Businesses That Don't Have Listed COGS?

Yes, there are businesses that do not have listed Cost of Goods Sold on their financial reports. Service businesses do not list Cost of Goods Sold on their income statements. Companies (law firms, consulting agencies, software developers) sell intangible expertise or digital access rather than physical products. Direct costs for the enterprises involve professional salaries and operating expenses. The costs appear in selling and administrative expenses on the financial report. A pure service firm lacks a physical inventory to track or value. Businesses (gyms, massage therapists) focus on labor and facility costs. Purely digital platforms (streaming services, social media networks) categorize server maintenance and development as operating costs. Standard accounting structures provide different formats for service entities. The absence of a physical product removes the need for inventory calculations. Many firms use a "Cost of Services" category to track professional time. The classification helps in determining the margin on billable hours. Managing a service business requires a focus on efficiency and billable utilization. Financial statements for the entities emphasize overhead and labor productivity. The lack of stock simplifies the tax reporting process. Every entity selects the appropriate reporting structure based on its primary revenue source. Precise categorization remains necessary for accurate tax filings. Service firms avoid the complexities of the standard cogs equation. Specialized strategies define the success of Companies for Customer Experience.

What are the Limitations of COGS?

The limitation of COGS are listed below.

- Inventory Tracking Difficulties: Maintaining precise records of physical stock poses a substantial challenge to growing businesses. Discrepancies arise from theft, damage, or human error during the counting process. Inaccurate data leads to misleading financial statements and incorrect tax filings.

- Accounting Method Variations: Different valuation techniques (FIFO, LIFO, Average Cost) produce varying results. Choosing a specific method influences the reported profit and the value of remaining stock. Inconsistent application of the methods complicates the comparison of financial performance.

- Profitability Misinterpretation: The figure accounts for direct costs and excludes operating expenses. A low value suggests high efficiency while ignoring high rent or marketing costs. Comprehensive analysis requires looking beyond the direct expenses to understand the true financial health.

Frequently asked questions about COGS

How Do We Calculate Cost of Goods Sold COGS? COGS = the starting inventory + purchases - ending inventory. Beginning inventory is the value of the product inventory that you started with. It's usually the same number recorded in the previous ending inventory. Purchases are usually the costs incurred during the reporting period, while ending inventory is the value left at the end of the reporting period.

COGS = the starting inventory + purchases - ending inventory. Beginning inventory is the value of the product inventory that you started with. It's usually the same number recorded in the previous ending inventory. Purchases are usually the costs incurred during the reporting period, while ending inventory is the value left at the end of the reporting period.

What Goes into the Cost of Goods Sold or COGS? These are direct costs involved in producing goods sold for your business. COGS includes directly used labor and the total costs of the materials used to create products. Additionally, other costs such as trade and cash discounts, freight-in, and total costs are included in this calculation. However, COGS doesn't include any indirect costs, e.g., sales forces expenses or distribution costs.

These are direct costs involved in producing goods sold for your business. COGS includes directly used labor and the total costs of the materials used to create products. Additionally, other costs such as trade and cash discounts, freight-in, and total costs are included in this calculation. However, COGS doesn't include any indirect costs, e.g., sales forces expenses or distribution costs.

What is cost of goods sold and how is it calculated? Costs of Goods Sold (COGS) represent the expenses involved into producing your goods over a certain period of time. The COGS formula is: COGS = the starting inventory + purchases - ending inventory.

Costs of Goods Sold (COGS) represent the expenses involved into producing your goods over a certain period of time. The COGS formula is: COGS = the starting inventory + purchases - ending inventory.

What are examples of COGS? Examples of COGS include the cost of raw materials, direct labor costs, and manufacturing overhead costs. In a retail business, the cost of the products purchased for resale would be considered COGS. For a service business, COGS may include the cost of supplies or labor directly associated with providing the service. Essentially, any costs directly tied to the production or purchase of goods or services sold by the business can be considered COGS.

Examples of COGS include the cost of raw materials, direct labor costs, and manufacturing overhead costs. In a retail business, the cost of the products purchased for resale would be considered COGS. For a service business, COGS may include the cost of supplies or labor directly associated with providing the service. Essentially, any costs directly tied to the production or purchase of goods or services sold by the business can be considered COGS.

If you liked this article, make it shine on your page :)